Interest rates, stamp duty percentages, and scheme details are indicative as of June 2026. Rates change. State stamp duty regulations are frequently revised. Always verify current rates at official bank websites and your state’s Registration Department before finalizing a transaction. FiiPay.in is not a home loan agent.

Banks love running ads about special home loans for women. They make it sound like you’ll get a big discount just for being a woman. The reality is much smaller.

The 0.05% rate saving is nice, but the real money is in stamp duty — often ₹1 lakh or more on Day 1. Most people I talk to completely miss the stamp duty part. That’s what this guide is actually about.

Is the Interest Rate Less for Women? The 0.05% Truth

Yes — it is lower. But the scale matters, and most people get surprised when they see the actual numbers.

Let’s be honest. Banks usually offer women a 0.05% to 0.10% concession on the interest rate. A few public sector banks occasionally go up to 0.25% under specific schemes, but that is rare.

On a ₹50 lakh loan, that’s roughly ₹236 less per month. Helpful, but not life-changing.

Why do banks do this? Data consistently shows women borrowers default less often. Lending to women is lower risk, so a slight rate concession makes business sense. It’s a calculated risk decision.

Use the 0.05% discount as a tie-breaker when comparing two banks. Never choose a bank exclusively for this if their processing fees are high or their customer service is poor.

Home Loan Interest Rate for Women vs Men: The Exact Savings

Let’s do the honest math instead of letting bank advertisements do it for you. Scenario: ₹50 lakh loan, 20-year tenure.

₹56,640 saved over 20 years sounds good until you realize stamp duty in many states gives you ₹1 lakh the same day you register the property.

📊 Rate Concession vs Stamp Duty (₹50L Property, Delhi)

The lesson: chase the stamp duty saving first. The interest rate concession is a bonus.

Lowest Home Loan Interest Rates for Women in 2026

These are indicative rates as of June 2026. Your actual rate will depend heavily on your CIBIL score and down payment.

| Bank / Lender | Scheme Name | Standard Rate (Men) | Women’s Rate | Concession | Processing Fee | Min. CIBIL |

|---|---|---|---|---|---|---|

| SBI | SBI HerGhar | 8.50% | 8.45% | 0.05% | Nil (up to ₹75L loans on campaign) | 750+ |

| HDFC Bank | HDFC Women Special | 8.75% | 8.70% | 0.05% | ₹5,000–₹15,000 or 0.25% | 750+ |

| ICICI Bank | ICICI Home Loan (Women) | 8.75% | 8.70% | 0.05% | 0.50% or ₹3,000 min | 750+ |

| PNB | PNB Pride (Women) | 8.40% | 8.30% | 0.10% | 0.35% or ₹2,500 min | 700+ |

| Bank of Baroda | BoB Mahila Home Loan | 8.40% | 8.30% | 0.10% | 0.25% or ₹2,500 min | 700+ |

| Central Bank of India | Cent Grih Lakshmi | 8.50% | 8.25% | 0.25% | 0.50% max ₹20,000 | 700+ |

| * Floating rates, repo-linked. Actual rate depends on CIBIL score, LTV ratio, and loan tenure. Verify before applying. | ||||||

The rate shown in bank advertisements typically applies to borrowers with a 750+ CIBIL, salaried income, and loan-to-value ratio below 75%. If your CIBIL is 690 or you’re self-employed, your sanctioned rate will be higher. The 0.05% women’s concession doesn’t overcome a below-average credit profile.

🏦 Central Bank of India — Cent Grih Lakshmi Scheme

Central Bank of India runs a dedicated home loan scheme for women offering one of the more meaningful concessions at 0.25% below the standard rate. The scheme is designed for women who are sole applicants or primary co-applicants with their husband. Key feature: women can apply even if their husband has an existing home loan in another city. Processing fee is capped and the scheme covers both construction and purchase.

💰 Calculate Your Exact EMI Difference

Compare standard vs women’s rate — see the exact monthly saving and total interest difference for your specific loan amount.

The “Reducing Balance” Math: How Interest Is Calculated

Most first-time borrowers assume the bank takes the total interest and splits it evenly across 240 months. That is not how loans work. Interest is calculated monthly on your outstanding principal. In the first few years, your EMI is almost entirely interest going straight to the bank.

Here’s what the first three months look like on a ₹50 lakh loan at 8.45% for a woman borrower:

| Month | Opening Balance | Monthly EMI | Interest Component | Principal Component | Closing Balance |

|---|---|---|---|---|---|

| Month 1 | ₹50,00,000 | ₹43,155 | ₹35,208 | ₹7,947 | ₹49,92,053 |

| Month 2 | ₹49,92,053 | ₹43,155 | ₹35,153 | ₹8,002 | ₹49,84,051 |

| Month 3 | ₹49,84,051 | ₹43,155 | ₹35,096 | ₹8,059 | ₹49,75,992 |

| After paying ₹1,29,465 in 3 months, outstanding principal has only reduced by ₹24,008. The remaining ₹1,05,457 went to the bank as interest. | |||||

This isn’t a scam — it’s mathematically how any loan works. But understanding it changes how you think about prepayment.

On a ₹50L loan at 8.45% for 20 years, making just one additional EMI payment per year effectively cuts 3.5 to 4 years off your loan tenure. This is why prepaying early makes such a big difference — you’re attacking the principal when interest is highest. Use the prepayment analyzer in our EMI Calculator to model your exact scenario.

Floating vs Fixed Rates: Which Should Women Choose?

Banks sell fixed-rate home loans as “peace of mind.” What they don’t always mention upfront is that fixed rates are typically 1%–1.5% higher than prevailing floating rates. Plus, true 20-year fixed rates are rare in India; most convert to floating after a few years anyway.

Since October 2019, all floating rate home loans are linked to an External Benchmark — usually the RBI Repo Rate. When the RBI cuts the repo rate, your loan gets cheaper. In today’s environment, most experts (and math) still favor floating rates for new borrowers.

When repo rates rise and your floating rate increases, banks have two options: increase your monthly EMI, or keep the EMI the same and extend your loan tenure. Most banks choose to extend the tenure. Your EMI statement looks the same, but your loan quietly became a 25-year loan instead of 20. Check your annual statement. If the tenure increased, ask the bank to raise your EMI instead to keep the timeline strict.

4 Factors That Define Your Actual Home Loan Rate

Factor 1: CIBIL Score — The Most Important Number

Your credit score overrides your gender. From what I’ve seen helping families in Himachal, a bad credit score overrides any gender discount. A woman with a CIBIL of 680 will get a worse rate than a man with a CIBIL of 760.

| CIBIL Score | Typical Rate Adjustment | Effective Rate (SBI Base 8.50%) |

|---|---|---|

| 750+ (Excellent) | Best rate available | 8.45% (women) / 8.50% (men) |

| 700–749 (Good) | +0.25% to +0.50% | 8.70%–8.95% |

| 650–699 (Fair) | +0.50% to +1.00% | 8.95%–9.45% |

| Below 650 (Poor) | Likely rejected or +1.5%+ | Often not sanctioned |

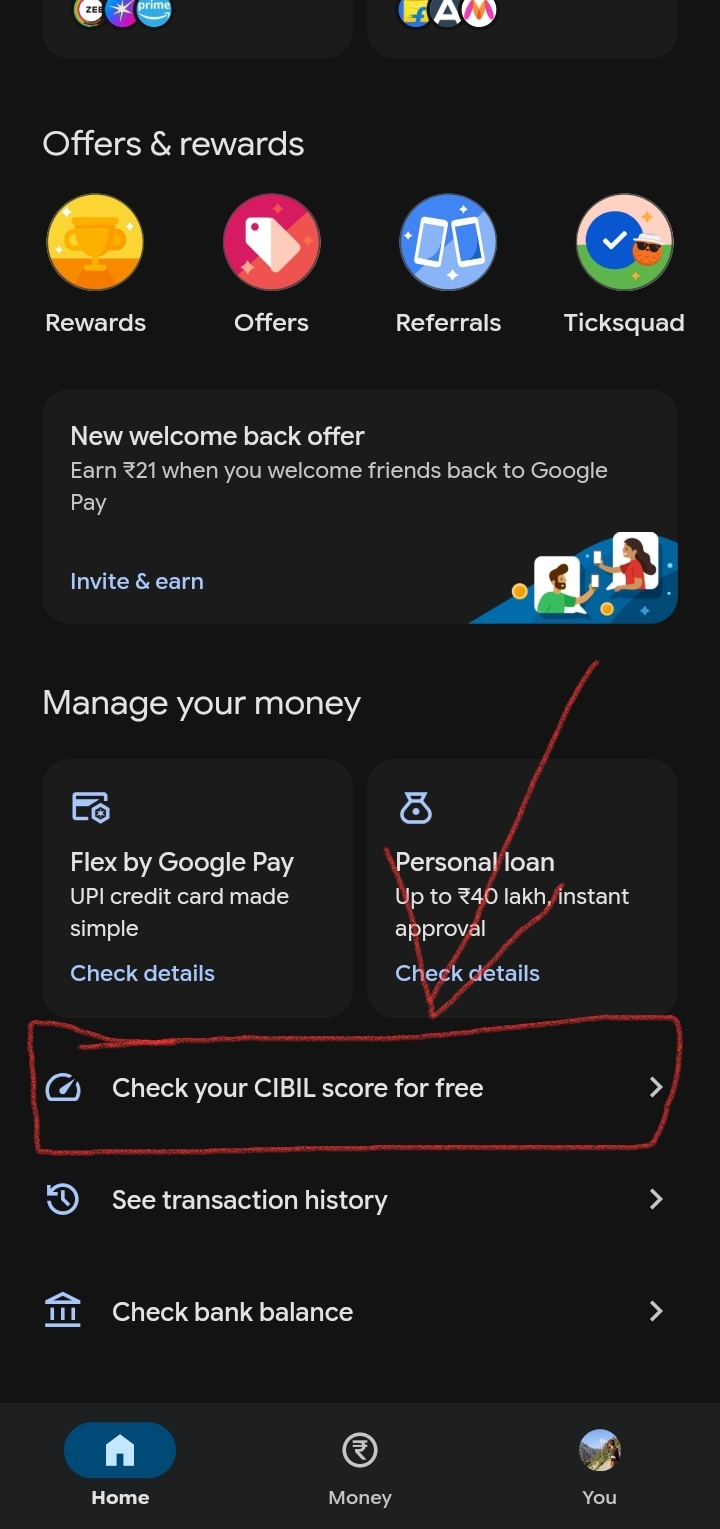

Step-by-Step: Check Your CIBIL for Free on GPay

Don’t fall for this common trap of paying for credit reports. You can check it securely on Google Pay.

- Open your Google Pay (GPay) app.

- Scroll all the way down to the bottom of the home screen.

- Click on “Check your CIBIL score for free”.

- Fill in your basic PAN details.

- Submit — your CIBIL score appears in seconds.

- This is a soft inquiry and won’t hurt your credit rating at all.

Tip: If your score is below 700, spend 6–12 months improving it before applying for a home loan.

Factor 2: Loan-to-Value (LTV) Ratio

LTV is the percentage of the property value you are borrowing. A 90% LTV (10% down payment) carries more risk for the bank. If you can increase your down payment from 10% to 20%, you secure a better rate and drastically cut total interest over 20 years. Park your savings in a high-interest FD while preparing to buy.

Factor 3: Salaried vs Self-Employed

Salaried women get the best rates because income is predictable via Form 16. Self-employed women face slightly higher rates (typically 0.25%–0.50% premium) because business income is variable. This is standard risk-based pricing, not discrimination.

Factor 4: Co-Applicant Rules

If a husband and wife apply jointly, the bank only grants the women’s rate concession if the woman is the primary (first) applicant. If the husband is listed first, the concession is routinely denied.

More importantly: if the wife is only a co-borrower on the loan but not a co-owner on the property deed, she gets zero stamp duty benefit and zero tax deduction eligibility. The property must be in her name for the financial benefits to apply.

The State-Wise Stamp Duty Discounts

This is where women (and smart families) actually make real money. Most states heavily discount property registration fees if the house is registered in a woman’s name.

| State / UT | Men’s Stamp Duty | Women’s Stamp Duty | Difference | Saving on ₹50L Property |

|---|---|---|---|---|

| Delhi | 6% | 4% | 2% | ₹1,00,000 |

| Haryana (Urban) | 7% | 5% | 2% | ₹1,00,000 |

| Punjab | 7% | 5% | 2% | ₹1,00,000 |

| Rajasthan | 6% | 4% | 2% | ₹1,00,000 |

| Himachal Pradesh | 8% | 4% | 4% | ₹2,00,000 |

| Uttarakhand | 5% | 3.75% | 1.25% | ₹62,500 |

| Uttar Pradesh | 7% | 6% | 1% | ₹50,000 |

| Madhya Pradesh | 7.5% | 5% | 2.5% | ₹1,25,000 |

| Bihar | 6.3% | 5.7% | 0.6% | ₹30,000 |

| Jharkhand | 4% | 3% | 1% | ₹50,000 |

| Maharashtra | 5% | 5% | 0% | No discount |

| Karnataka | 5% | 5% | 0% | No discount |

| Tamil Nadu | 7% | 7% | 0% | No discount |

| Gujarat | 4.9% | 4.9% | 0% | No discount |

| Andhra Pradesh | 5% | 5% | 0% | No discount |

| Telangana | 5% | 5% | 0% | No discount |

| Kerala | 6% | 6% | 0% | No discount |

| West Bengal | 5% | 4% | 1% | ₹50,000 |

| Odisha | 5% | 4% | 1% | ₹50,000 |

| Chhattisgarh | 5% | 4% | 1% | ₹50,000 |

| * Indicative rates for 2026. States revise these frequently. Always verify at your local Sub-Registrar’s office. | ||||

In states like Haryana and Himachal Pradesh, simply ensuring the woman’s name is first on the sale deed saves between ₹1 lakh and ₹2 lakh instantly. Combine this upfront cash saving with the interest rate concession for maximum impact.

State-Wise Women Home Loan Schemes — Where to Apply

| State / UT | Scheme / Program | Offering Bank / Agency | Key Benefit |

|---|---|---|---|

| All India | SBI HerGhar | State Bank of India | 0.05% rate concession; women primary applicant |

| All India | Cent Grih Lakshmi | Central Bank of India | 0.25% rate concession; women-only scheme |

| All India | PMAY-U (EWS/LIG) | All scheduled banks | Female ownership mandatory for subsidy |

| Himachal Pradesh | HPSCB Housing Loan for Women | HP State Cooperative Bank | Concessional rate + rural focus |

| Delhi | DDA Housing Scheme (women priority) | Delhi Development Authority | Priority allotment; lower stamp duty |

| Maharashtra | Maha Gharkul (EWS Women) | Maharashtra government | EWS women: subsidized housing |

| Tamil Nadu | TIDCO Housing (Women Priority) | TIDCO / nationalised banks | Women-headed household priority allocation |

| Kerala | KSFE Home Loan for Women | Kerala State Financial Enterprises | Low-interest cooperative finance |

| Rajasthan | RHBAS Housing Scheme | Rajasthan Housing Board | Women applicant priority |

| West Bengal | WBHB Women’s Housing | West Bengal Housing Board | Priority queue for female-headed households |

| Punjab | PNB Mahila Housing Loan | Punjab National Bank | 0.10% concession + Punjab stamp duty saving |

| Haryana | BoB Mahila Home Loan | Bank of Baroda | 0.10% rate + Haryana stamp duty saving |

| Gujarat | GRUH Finance / HDFC Women | HDFC / GRUH | Flexible income assessment for MSME women |

| Karnataka | KSFC Women Entrepreneurs | Karnataka State FC | For self-employed women |

| Andhra Pradesh | APSFL Women Housing | AP State Finance / banks | EWS women priority |

| Telangana | KCR Kit + Housing Scheme | State government + banks | Government housing subsidy for BPL women |

| Uttar Pradesh | UPSIDA Women Housing | UP State Industrial Dev. Auth. | EWS/LIG women housing |

| Bihar | BSPHCL Women Scheme | Bihar State Housing Corporation | State-subsidised housing |

| Odisha | MO GHARA (Women Priority) | Odisha government / banks | Rural + urban housing; women-first allotment |

| MP | MP Mahila Awas Yojana | MP govt + UCO / SBI | Women-headed household priority |

| Jharkhand | JRDA Women Housing | Jharkhand RDA | Tribal and rural women housing priority |

| Chhattisgarh | CG Mukhyamantri Awas Yojana | State + banks | Female registration mandatory for subsidy |

| Assam | APDCL Women Scheme | Assam Housing Board + SBI | Rural women; low documentation requirement |

| Uttarakhand | UAKVN Women Housing | Uttarakhand Nagar Vikas Nigam | Hill region women priority |

| Goa | Goa Housing Board | Goa Housing Board | Standard PMAY applicability |

| Chandigarh (UT) | CHDP Women Priority | Chandigarh Housing Board | Women of weaker sections priority allotment |

| J&K (UT) | JKERA Women Housing | J&K Economical Reconstruction Agency | Women-headed household priority |

| Puducherry (UT) | PITCL Women Housing | Puducherry ITD + banks | Women-only plots in select layouts |

| * Scheme availability changes with state budgets. Verify the current scheme at the respective bank’s branch or state government website before applying. | |||

🏔️ Spotlight: HP State Cooperative Bank

The Himachal Pradesh State Cooperative Bank (HPSCB) offers a dedicated housing loan scheme for women with HP domicile. It features a concessional interest rate and relaxed collateral norms for rural applicants. This is highly relevant for women in Shimla, Kangra, Mandi, and Chamba. HPSCB branches in smaller towns often have faster processing than commercial banks for rural applicants.

How to Negotiate at the Bank Counter

Never accept the first offer. I’ve seen people save another 0.10% just by showing a better quote from another bank. Get a formal sanction letter from SBI and take it to HDFC. Let them fight for your 20-year business.

Processing fees (usually ₹12,500 to ₹25,000) are highly negotiable. Branch managers have the authority to waive them entirely, especially at quarter-end. Ask directly for a complete waiver.

Banks will aggressively push “Credit Shield” life insurance. It is illegal for a bank to force you to buy their insurance to get a loan. Buy an independent term plan online; it costs 30-50% less.

Banks are required to pass on RBI repo rate cuts, but many don’t proactively notify existing borrowers. Every time RBI cuts rates, call your bank and request a rate reset confirmation.

Calculate Your Exact EMI and Savings

See exactly how much the 0.05% women’s concession saves you.

Frequently Asked Questions

Final Verdict

The interest rate discount for women is a nice advantage, but it’s not everything. Here is the exact order of priority you should follow:

- Fix your CIBIL Score: Build it past 750. This dictates your baseline rate.

- Focus on Stamp Duty: Register the property in the woman’s name to instantly save ₹1 lakh to ₹2 lakh upfront.

- Waive Processing Fees: Negotiate them down to zero.

- Claim the Rate Concession: Ensure you get the 0.05% discount applied properly.

Do the math properly. Register the property in the woman’s name. Negotiate hard. The small rate concession is just the cherry on top.

This article is strictly for educational purposes. All rates, policies, and stamp duty percentages reflect data available as of June 2026. Banks and state governments revise these figures constantly. We strongly advise verifying current stamp duty laws at your local Sub-Registrar and confirming interest rates with your bank branch prior to application. FiiPay.in operates as an independent financial research platform and is not a registered loan agent or financial advisory firm.